Blog

/

BaaS 101

What’s an FBO Structured Partnership Model Versus an On-Core Structure?

Insights into the strategic choice between FBO and on-core banking structures.

Key Takeaways:

- FBO Structure: Offers more control and customization for fintechs focused on financial tools as core offerings but comes with more responsibility regarding compliance, fraud prevention, and support.

- On-Core Structure: Provides a more streamlined, maintenance-free approach with direct access to the partner bank's services but less customization, better for those embedding financial features as a secondary offering.

- Choosing Your Path: Determining whether to integrate deeply with on-core accounts or leverage the flexibility of an FBO account depends on your product vision and operational capabilities.

Whether you’re embedding banking tools into an otherwise non-financial app or building a neobank, you’ll have to make a critical choice early on between two basic partnership structures with a bank: FBO or on-core.

Your decision here matters tremendously to your overall business and product strategy. The type of structure you decide to build could determine what features you can offer, how fast you can add new features, how much control you have over your product, and how much you must work to maintain accounts.

If you choose to leverage the banks in a more integrated way and open individual end user accounts directly on their platform, that means your customers are opening accounts on your partner bank’s core. Your other option is to open one big fiduciary account on the bank’s core, then provide customers with virtual accounts that exist within that larger account. This second option is referred to as a “for benefit of” or FBO structure.

Neither option is better than the other, but they each come with different benefits and different features. Depending on your product offering and goals, one form of account structure will be the best option for your unique needs. To provide top-of-line service to all client companies, Treasury Prime offers both FBO and on-core options.

To learn more about how dedicated vs. intermingled FBO accounts, watch our on-demand webinar.

What is the difference between FBO and on-core banking?

At a high level, on-core accounts allow you to leverage the bank’s existing infrastructure in a meaningful way and lead to potentially less work or obligations to open and maintain. However, the clear offset to this is a potentially limited ability to customize certain features of a product offering. A great on-core use case could be a white-labeled or co-branded non-fintech embedding bank accounts in their product as a side perk, or just offering one or a couple of peripheral financial tools.

FBO accounts, on the other hand, require more responsibility from the company managing the account, but also allow for greater customization. The FBO route can be attractive for companies offering bank accounts and various financial tools as central features in their product.

Here’s a more detailed comparison.

What are on-core accounts?

On-core account quick facts:

- Why is it called an on-core account? On-core accounts are accounts opened directly on a bank’s core, or back-end system.

- Where have you seen on-core accounts before? Ever opened a checking or savings account directly with your local bank? Well, this account is likely housed and recorded on their primary core platform just like in the model discussed here.

How on-core accounts work

When you opt to offer on-core accounts in your app, the accounts exist directly on the bank’s back-end system for processing daily transactions. That means accounts can potentially do everything the bank’s core allows — and also only what that core allows. Some examples of settings that are commonly global across a bank's platforms are KYC decisioning, onboarding procedures, incoming funds holds times/rules, overdraft settings, account fees or incoming ACH decisioning. Additionally, the bank has greater visibility into account activity, which allows the bank to participate in customer support and simplifies compliance. Compliance refers to processes that help fintechs and banks stay in line with any number of laws, regulations, or rules imposed by regulators or industry self-regulating organizations.

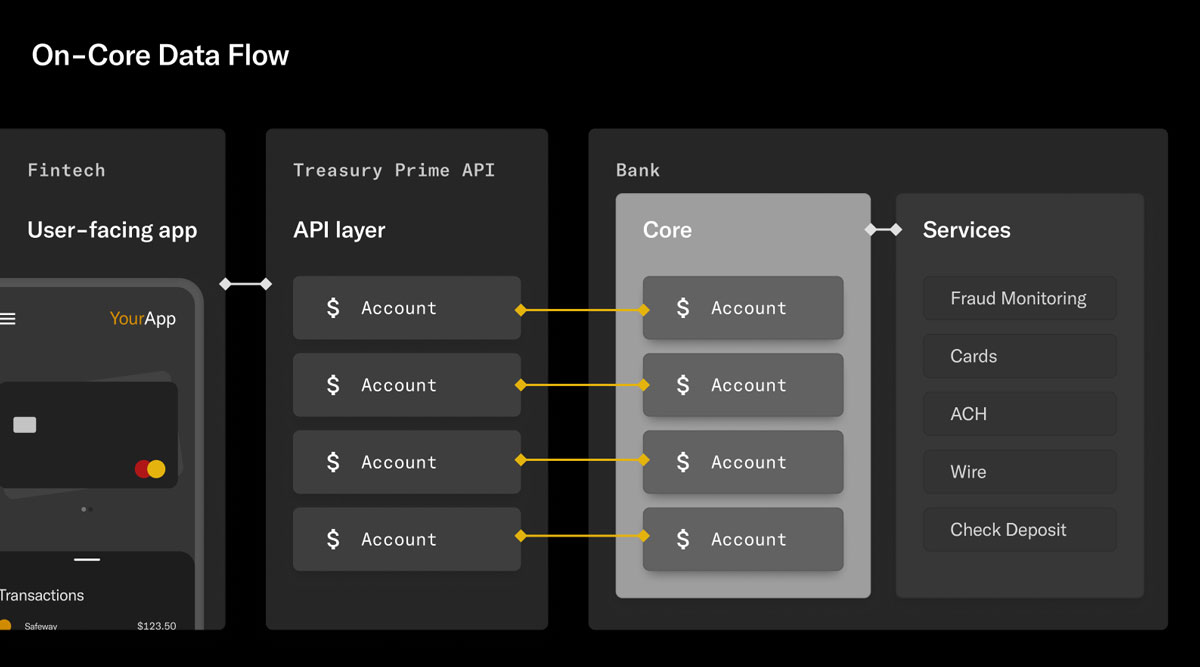

On-core data flow

In an on-core setup, users interact with their accounts through the user-facing app you have built. The app connects to a banking API layer, which interfaces directly with the bank’s core and, in turn, the bank’s services.

What is an FBO account?

FBO quick facts

- What does FBO mean? FBO stands for “for benefit of.” An FBO account is an umbrella account that holds the aggregate deposit balances for multiple accounts held on a separate ledger. Banking as a service (BaaS) providers sometimes refer to FBO accounts as ledger accounts because they typically use a ledger service to track and record account-level activity.

- Who is the owner of an FBO account? This may sound counterintuitive, but the fintech has no ownership interest in the FBO account and has no controlling rights to funds. The funds in the FBO are owned and subsequently controlled by the end users. Those funds are held at the bank for the benefit of a company’s clients. No money movement in or out of that account should take place unless it is instructed by or because of an end user’s actions.

How an FBO account works

An FBO setup works differently from an on-core setup because it creates a flexible integration layer between your customers and the bank’s core. Rather than your customers opening accounts directly on the bank’s legacy core, they open virtual accounts within the FBO structure. This allows for greater freedom for account customization and feature enhancements because you would not be tied to some of the traditional settings or rules that have been instituted on the bank's core to accommodate their traditional business lines.

There are two ways to operate an FBO setup depending on your BaaS provider.

- Traditional "dedicated FBO" approach: The traditional and less risky approach is for the BaaS provider to open a discrete FBO account for each company it partners with. Under this approach, you have your own dedicated FBO account from which to carve virtual accounts for your customers. This is the approach Treasury Prime uses.

- Alternative “intermingled FBO” model: Some BaaS providers offer an intermingled FBO model. In this alternative model, the BaaS provider opens one FBO account to service all of its company clients, rather than have each company open an FBO account with the partner bank directly. This arrangement basically means you are sharing risk with other companies, and also that you are all subject to the same one-size-fits-all KYC and compliance operations. In short, this second option can come with higher risk.

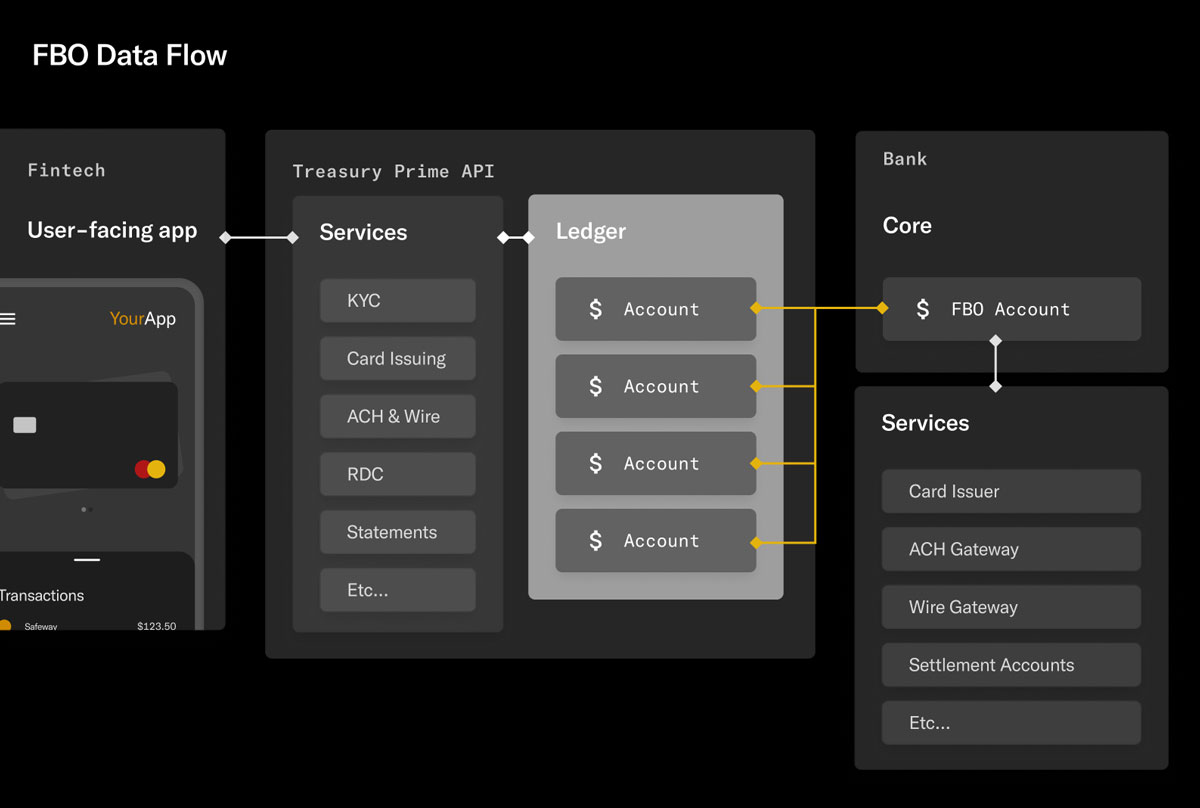

FBO data flow

In an FBO setup, users interact with their accounts through the user-facing app you have built. The app connects to a banking API layer, which contains a ledger where records of user account activity are held. The ledger is built on top of an FBO account. That FBO account exists on the bank’s core and attaches to the bank’s services.

For greater control and flexibility, choose FBO

FBO accounts essentially create a platform for innovation. That power comes with greater responsibility. If you’re building a neobank or an app that centers financial tools, the effort may be worth it.

Benefits of an FBO account

- More control over KYC & account approvals: In an on-core setup, your partner bank performs essentially all typical bank services. That means the bank decides whether to approve certain customers, not you; and the bank decides what forms of identification it will accept for KYC. This can limit who you can accept as a customer. In an FBO model, those services can be performed by you with support from the BaaS provider and other compliance partners, and you have more flexibility based on your specific user base and customer risk profiles.

- Faster account opening: Because you have control over the process for opening your customers’ virtual accounts, you can do so faster.

- Can be less expensive than on-core

- More latitude to customize and innovate: Your FBO account holds your customers’ virtual accounts, which means you and your BaaS provider can collaborate on what features you want to offer.

- Easier to mitigate bank partner risk: No one wants to pick a bank partner and build a successful program with them just to rip it all down to move banks. However, sometimes this hard truth is a reality for many reasons that you may not always be able to control. Treasury Prime accounted for this possibility and built its technology to be bank agnostic. So if you need to switch banks you would not need to rebuild your tech stack, change bank account numbers or learn new procedures. While some things just can’t be automated, like a change in routing number or end-client acknowledgment of the change, we have made it as painless as possible. .

Drawbacks to FBO account

- Increased support responsibility: Because your FBO account holds your customers’ virtual accounts, you are responsible for servicing them. If your customers opened accounts directly on your partner bank’s core, the bank could fully service them.

- Increased reporting requirements: Similar to having increased responsibility for supporting customers’ accounts, you will also be responsible for staying in compliance by reporting information and activity to authorities such as the FDIC.

- Greater responsibility for fraud prevention: Your partner bank can’t see what’s happening within your customers’ virtual accounts. That means it’s up to you to monitor accounts for potential fraudulent activity.

For a more hands-off approach, choose on-core

On-core accounts require less maintenance from you as an app developer and allow you out-of-the-box access to all of your partner bank’s account services. That said, your features may be limited with this setup. But if you’re embedding financial tools to enhance your app, rather than making them central, on-core accounts can get the job done with less hassle.

Benefits of on-core accounts

- All of the bank’s account services out-of-the-box: Your customers essentially have traditional accounts with your partner bank, granting them all the bells and whistles that come with that, without you having to build out those features.

- Bank-grade KYC and fraud detection: You can leave the process of approaching applicants for accounts and monitoring accounts for fraudulent activity up to your bank.

- Extra customer support: Because customers have accounts directly with the bank, they can go to the bank for customer support needs that involve account-level issues.

- Maintained by the bank partner: The bank maintains accounts and updates them as needed.

Drawbacks of on-core accounts

- Inflexible: Customer accounts opened on-core must follow all bank policies, and can only offer features the bank permits. Ultimately account offerings are dependent on the bank’s existing services and processes.

- Less control over KYC & account approvals: When customers open accounts directly with the bank on-core, it’s up to the bank what forms of identification to accept and which account applicants to approve.

- Slower account opening: Whereas with an FBO account you can just issue a virtual account when ready or necessary, with an on-core account your customer must go through the full process your partner bank uses to open accounts.

- Bank core technology limitations: When accounts are opened on-core, their features are limited to what the bank’s core can handle from a technology standpoint.

Compliance considerations - Bank account level of risk

The biggest difference between on-core and FBO solutions is the tools you need to maintain compliance in collaboration with your bank partner. When accounts are on-core, you can rely more heavily on your bank partner to help take care of regulatory and fraud prevention requirements stemming from the traditional bank account level of risk. When you go the FBO route, you have to participate with your own processes and take extra steps to provide the bank with any visibility it needs into accounts.

Finding the right BaaS provider is always critical. You need a partner who will guide you toward the account setup option that meets your highest needs. You also need a partner who will facilitate a direct relationship between you and your bank. But the right provider becomes even more crucial when you are dealing with an FBO account, which can be riskier.

Look for a BaaS provider who offers these tools and approaches for managing FBO accounts:

- You have your own separate FBO account at your partner bank instead of being grouped with other companies.

- Appropriate transaction monitoring tools are integrated

- Adequate KYC, tailored to your needs, established for end users and your company

Treasury Prime offers all these tools for FBO accounts. With these safeguards in place, your compliance and risk management setup for your FBO account can be just as rigorous and secure as it would have been had you gone the on-core route. In that way, should you need the flexibility of an FBO account to build the best product, you can have the best of all worlds.

Treasury Prime is unique in the BaaS provider space in that we work with a network of bank partners in offering both FBO accounts and on-core accounts to our fintech and embedded banking partners. We have just launched a new compliance solution empowering fintechs to build and launch risk-based compliance programs in weeks. Our partners include leading vendors in the space such as Alloy and Unit 21.

Want to dive deeper on compliance? Watch this on-demand webinar with Treasury Prime VP of Compliance Solutions Sheetal Parikh. To learn more about how Treasury Prime can help your bank or fintech grow through collaboration, get in touch with our team.

Related embedded banking content:

5 Reasons a BaaS Provider with a Large Banking Network Can Boost Your Botton Line and Mitigate Risk

Share

Share