Blog

/

Compliance

EAT or be eaten: Defining the AI compliance conversation

Earlier this month, our team attended the American Fintech Council's Risk and Compliance conference in Washington, D.C., a room with the right cross-section of the industry: sponsor bank executives, and fintech operators representing the FDIC, OCC, and Federal Reserve.

Topics spanning third-party risk management, agentic AI, and what financial services regulation looks like in 2026.One theme cut through every single session; Not model accuracy, not implementation cost, not even the thorny question of vendor liability.

The biggest barrier to AI adoption in financial services right now is explainability: can a compliance team explain and defend the AI decisioning process to a regulator standing over their shoulder? what we're building at Treasury Prime.

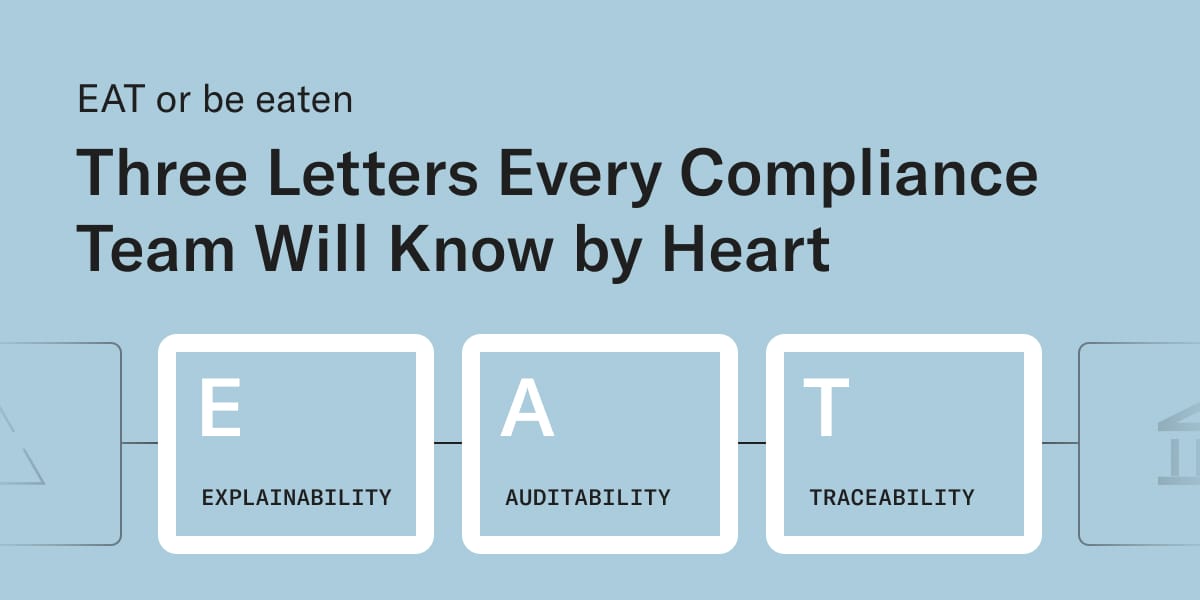

Three letters every compliance team will know by heart

Our summary of the key takeaways were:

- Explainability. A plain-language description of why the system made the decision it made, legible to a non-technical examiner. Banks are accountable for AI-driven outputs the same way they're accountable for human ones.

- Auditability. A durable, complete decision trail, even when that decision process touched five models across three processing steps. Systems that don't build this in from the start will get it retrofitted, badly, later, at significant cost.

- Traceability. What data, when, and what flowed from it. Regulators are zeroing in on data provenance as AI systems draw from far broader inputs than traditional rule-based logic ever did.

EAT is not a checklist. It is the threshold test for whether a Compliance team will allow their bank to deploy AI at all, and whether they'll extend that permission to their fintech partners. The AFC itself has been explicit about this direction. In a June 2026 letter to federal banking agencies, AFC CEO Phil Goldfeder called for regulators to "establish clear, predictable, and collaborative compliance standards that embrace innovative tools rather than relying on outdated, manual, and procedural requirements that increase costs without improving outcomes."

For anyone building in the BaaS space, the implication is direct: EAT is infrastructure. You cannot bolt it on after deployment and you cannot win deals without it. See how compliance-first infrastructure works in practice →

There's no wall between you and your bank when the regulator walks in

One of the more encouraging signals from the conference: fintechs are arriving at bank partnerships meaningfully better prepared on compliance than they were two or three years ago.

The old failure mode was predictable. Treat compliance as the bank's problem. What's emerging in its place is a recognition that a fintech operating inside a bank's program isn't adjacent to the bank's compliance framework.

The question banks are now asking their fintech partners has changed. It's no longer "do you have a compliance program?" The question now is "can you demonstrate your compliance processes and share your compliance policies. When a regulator comes knocking, the bank is on the hook regardless of where the compliance policy came from, or even where the AI decision originated.

The infrastructure conclusion: the compliance responsibilities in a bank-fintech relationship is shared. A fintech's audit log and a bank's audit log shouldn't be different documents reconciled after the fact. They should be the same document, in real time, accessible to both parties. Infrastructure that doesn't support that model isn't AI-ready, it's a liability waiting to be discovered at the most untimely point.

Reading between the lines at the Fed, FDIC, and OCC

The FDIC, OCC, and Federal Reserve panel was encouraging - through the desire to enable all financial institutions to innovate, while also being open minded about leveraging AI to enable that innovation.

Regulators expressed direct concern about the emergence of a two-tier financial system, one where only the largest institutions have the compliance infrastructure to justify AI investment at all. The worry isn't just JPMorgan's head start. It's what happens to the rest of the banking system if that gap compounds. Our 2025 Banking Innovation Index found that community banks are already feeling this pressure firsthand. For infrastructure providers, that's not just an observation. It's a mandate. Making EAT-compliant AI accessible to institutions of every size is the market opportunity regulators are signaling they want to see filled.

The second signal was about standardization. Regulatory offices are actively building their own AI capabilities and investing in upskilling national offices to drive a consistent compliance message across institutions. The direction of travel isn't toward a more permissive environment. It's toward a more uniform one. AFC Chief Policy Officer Ian Moloney put it directly in a June 2026 comment letter to federal banking agencies: "Effective AML/CFT supervision should focus on identifying and mitigating meaningful risks rather than measuring compliance through procedural checklists." The regulators in the room at AFC's own conference were signaling the same thing. The checklist era is ending. The accountability era is beginning.

The window is open. It won't stay open indefinitely. The banks and fintechs that treat this moment as an implementation runway rather than a waiting period are the ones that will be in the room when the standard sets, rather than scrambling to catch up to it.

Stop trying to route around compliance. Build what it needs.

The real takeaway from the AFC conference: compliance teams aren't blocking AI adoption out of conservatism. They're being asked to sign off on systems they can't yet defend to their regulators, and they're right to pause.

The opportunity is to build the infrastructure that gives them what they need to say yes. EAT isn't a compliance tax on AI development. It's the foundation that makes AI adoption durable, and the bar that separates infrastructure worth building on from infrastructure that will get replaced.

Banks that build this now will be positioned to move decisively when their fintech partners are ready and when regulators expect them to be. That's the market we're building for.

Treasury Prime is building AI services and tools that embrace EAT from their initial foundation, to help automate and augment the most tiresome tasks that Banks need to complete. We are excited about the future of financial services and looking forward to partnering with you on that journey.

Read our white paper on AI-ready banking infrastructure → or reach out to our team directly.

Share

Share