Blog

/

Product

Getting Your Bank Ready to Launch Fintech Partnerships with Treasury Prime

When a bank decides to partner with Treasury Prime, it is embarking on a brand new approach to fintech innovation and revenue generation. This is a big step forward and it’s important to choose a banking as a service provider that understands risk and knows how to integrate with bank systems smoothly.

Our founders and other team members have deep experience working inside banks and developed the Treasury Prime API software specifically with banks’ needs and systems in mind. The Treasury Prime team takes a hands-on approach to ensure banks are supported every step of the implementation process, all the way through to launch with their first fintech or enterprise partners.

Why partner with Treasury Prime

As more and more fintechs and enterprises look to embedded finance to open up new revenue streams and attract new customers, banks are looking to do the same. Banking as a service providers equip banks with the tech that makes it possible for them to integrate with the fintechs and enterprises that are hungry for bank partners.

What’s in it for banks? New lines of business and the opportunity to bring in low to no-cost deposits and significant fee income — and doing so without heavy internal investment in revamping systems or tech stacks.

For banks, adding BaaS can be the modern-day equivalent of adding branch locations – without much capital expenditure. It allows them to dramatically reduce the cost of new deposits (Oliver Wyman estimates with a new BaaS technology stack, the cost of acquiring a customer ranges from $5-$35, down from $100-$200) while increasing potential revenue from fees.

A BaaS provider like Treasury Prime supplies not only the technology that enables banks to modernize their infrastructure, but also shepherds the relationship with fintechs and enterprises so that banks can increase top-line revenue and diversify their portfolio more easily.

If you're a bank wanting to modernize the way you do business and seamlessly integrate with fintechs and other enterprises, contact us.

Implementation process

The implementation timeline for banks can differ depending on which banking core they’re on. If a bank is already on a core that Treasury Prime integrates with, such as FIS, IBS, or Horizon, it can take as little as a few weeks.

For banks on a new core to Treasury Prime, the implementation process typically takes about 8-12 weeks. This includes development time from the Treasury Prime team and time for the bank to conduct due diligence and to work through any internal processes to ready themselves for the integration. Once integrated the bank and Treasury Prime can turn on new fintechs in weeks.

This is compared to the possible 6 months to a year or more that it can take for a bank to launch a new digital financial service on its own or with a traditional software provider. A huge priority for Treasury Prime is to cut down the timeline for getting to market significantly for both banks and fintechs.

Implementation for banks can generally be broken down into the stages below. At every step of the process, you’ll have a direct line of contact with the Treasury Prime team.

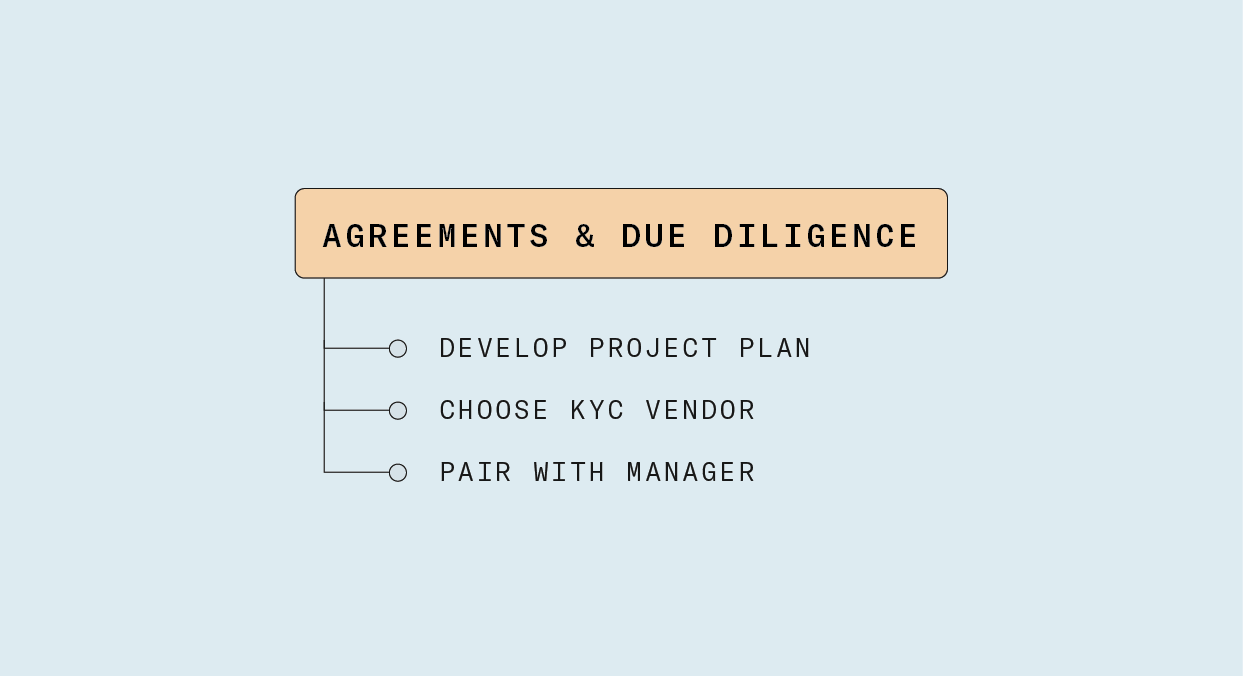

Step 1: Agreements and due diligence

After speaking to our sales team, banks will move on to signing the necessary agreements to get the implementation process started. These include a letter of intent (LOI) and master service agreement (MSA).

At this stage, we’ll also work with the banks to determine a sample project plan. Banks will be able to choose a KYC vendor and transaction monitoring vendor. At Treasury Prime, we work with Alloy as our KYC vendor partners. We also partner with Unit21 for real-time transaction monitoring. Banks also have the freedom to choose to work with different vendors they choose.

Banks will also be assigned an implementation manager who will be their point of contact to answer any questions, provide guidance, and to generally facilitate the onboarding process.

Step 2: Pre-Kickoff

Once documents are signed and due diligence is completed between all parties, a pre-kickoff meeting is usually scheduled between any project managers and the Treasury Prime team to brief them on what to expect as the process moves forward. Once the bank team is briefed, a series of calls will begin to regularly occur, at least once a week. These calls will cover important topics like compliance, funds flow, and project scope.

Concurrently, the Treasury Prime team will also create test accounts to trial different functionalities and connections to the bank's core.

Step 3: Kickoff implementation

With process infrastructure and testing in place, the beginning stages of development and implementation will be underway.

Banks should be prepared to facilitate providing access to their banking core API documents to Treasury Prime at this time. Treasury Prime will work with the bank and core provider to run pertinent production tests to make sure the integration is successful.

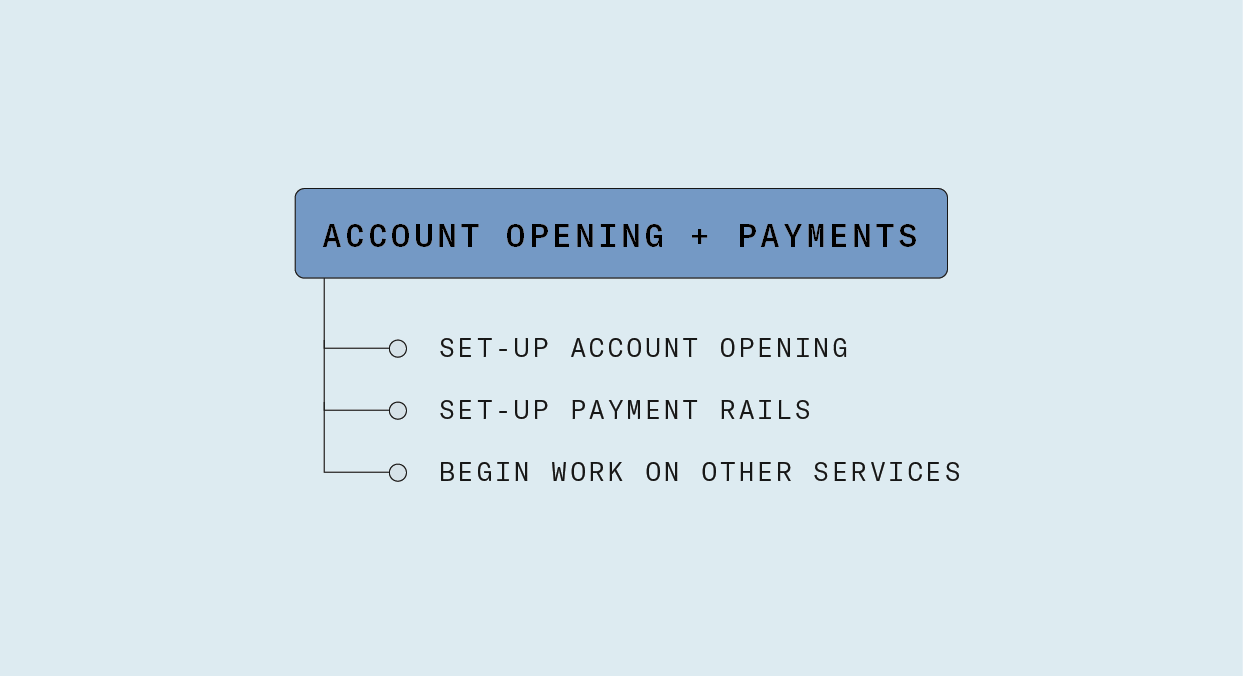

Step 4: Account opening and payments

With development finished, the bank and Treasury Prime will work together to determine the Know Your Customer (KYC) setup and account opening parameters.

At this stage, Treasury Prime will also set up payment rails — like ACH and wires — for the bank to be used between them and the fintechs they’ll partner with. As the payments programs are developed, Treasury Prime will work with the bank team to launch other desired services like card issuing in the future.

Step 5: Post-implementation

Once fully integrated with Treasury Prime, the bank’s dedicated implementation manager will then hand off the reins to a dedicated relationship manager. The relationship manager is responsible for ensuring partner banks are getting everything they need by way of product updates and releases, bug fixes, day-to-day operations, as well as monthly and quarterly business reviews with the bank’s top executives to discuss upcoming goals and objectives.

After full implementation, the bank will be ready to partner with its first fintech or enterprise customer.

Finding the right fintech

Many Treasury Prime team members have years of experience in the banking and finance fields, so while we won’t provide any legal counsel, our team is prepared to provide advice on what makes the most sense for the bank at any stage in their relationship with us. And with our compliance solution in place, we can also ensure that we’re not only recommending partners who are a great fit for the bank but have also passed initial background checks to be safe to do business with. Treasury Prime’s regulatory compliance experts are uniquely positioned to accommodate the competing interests created by an increasingly onerous regulatory environment governing banks with the sense of urgency to get to market that is a business requirement for many fintechs and enterprises.

Once Treasury Prime introduces or a bank identifies a fintech they’d like to work with, the dedicated relationship manager will work with the corresponding fintech’s customer success manager to ensure the partnership is ushered through to completion.

Getting started with Treasury Prime

Working with a BaaS provider can unlock many different ways for a bank to thrive, particularly at a time when enterprises are looking for new ways to increase revenue and diversify their offerings.

And joining a BaaS provider like Treasury Prime that has a leading product and team dedicated to implementation and partnerships means any bank can join this movement at unprecedented speed and ease.

If you’re ready to get started, we’d love to hear from you. Contact us.

Share

Share